Thank you, it's cool. Used for the first time because only then was the right drug. Very revealing detail: ordered Express shipping to get the order within 3 hours because didn't know how to get the order faster https://africarx.co.za/buy-levitra-south-africa.html The drug is authentic exactly. Consistent with the stated prices the Staff is knowledgeable.

Microsoft word - english_20120713-formatted.doc

Retail Market Monitor (Hong Kong) 13 July 2012 From the Regional Morning Notes The United Laboratories (3933 HK/BUY/Target: HK$5.00) Sales Volume Of Bulk Medicine Rebounds; Expect Positive Earnings In 1H12 What’s New The United Laboratories (TUL) saw a rebound in the sales volume of major bulk medicine and is expecting positive earnings in 1H12. Stock Impact 1H12 sales volume rebounded. According to management, TUL’s sales volume of 6-Aminopenicillanic acid (6-APA) and amoxicillin rebounded by about 10% yoy in 1H12. We see the volume growth as a positive signal for TUL’s market expansion plans. We foresee the trend continuing as an increasing number of antibiotic producers exit the market. Prices of bulk medicines stabilise and are unlikely to drop further in 2012. Our industry checks reveal that prices of intermediate products and bulk medicine, eg, 6-APA, 7-AminoCephalosporanic acid (7-ACA) and amoxicillin have reached the industry cost levels seen in 4Q11. We saw a slight price increase in 1H12 from 4Q11. We believe bulk medicine prices will remain low but are unlikely to fall much further in 2012. Insulin revenue soars and will generate significant revenue contribution in the next 2-3 years. According to data, there are more than 100m patients suffering from diabetes in China. The main drug, recombinant human insulin, has a market value of about Rmb6b in China and is growing rapidly at a CAGR of over 20%. TUL has invested Rmb1b in an attempt to tap the fast-growing recombinant human insulin market. According to management, revenue from insulin products was about HK$9m in 1Q12, increasing substantially compared with about HK$14m for the full year in 2011. We are optimistic about the management’s target of achieving a revenue of HK$50m in 2012 and HK$100m in 2013. Assuming the tender price (currently about Rmb45/unit) will remain relatively stable, we expect insulin products to generate significant revenue contribution of about 5% in 2015. Maintain BUY, and target price of HK$5.00, based on our discounted cash flow model, assuming WACC of 10% and the terminal growth rate of 2%. The target price implies 1.2x 2012F P/B. After suffering a loss in 2H11 due to the impact of restrictions on the use of antibiotics and sharp price declines in bulk medicine, TUL is now gradually recovering from the industry downturn by strengthening its marketing strategy and expanding market share of its new products.

Technical Analysis

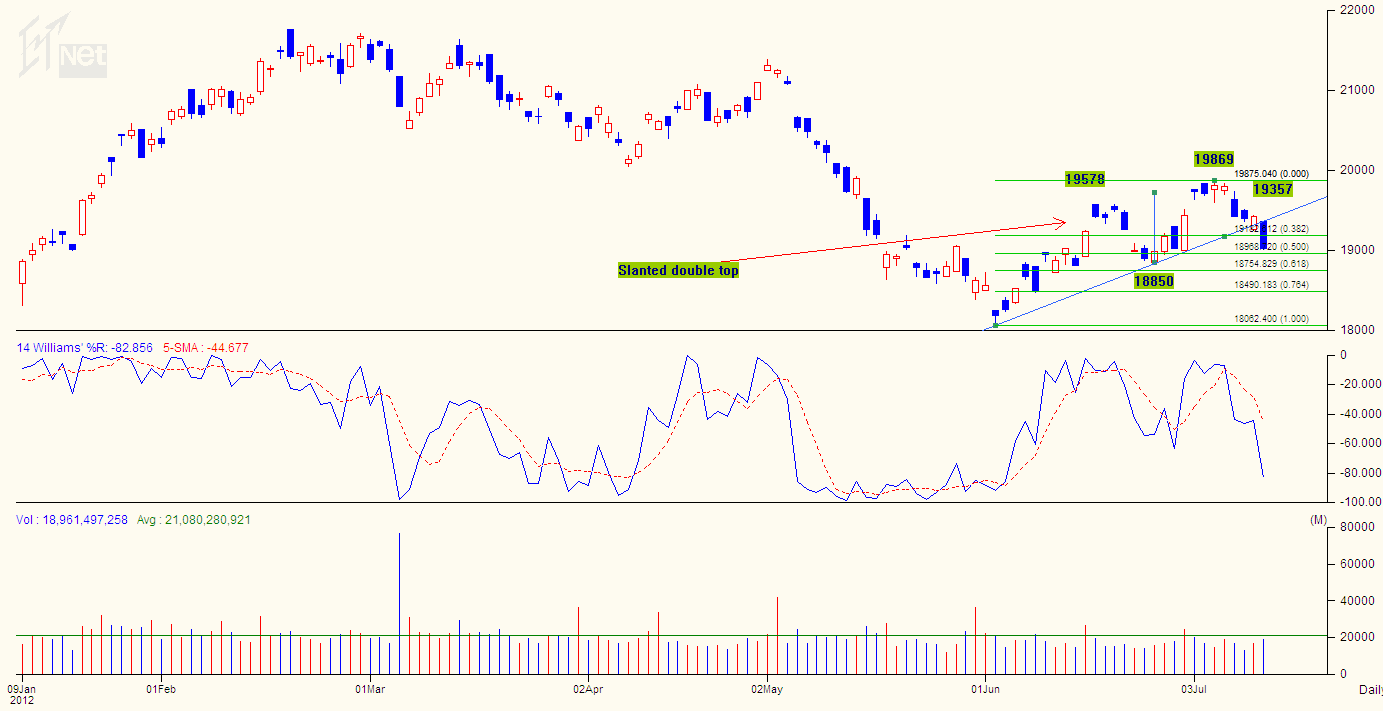

Hang Seng Index: Testing support at 18,483

Since the Hang Seng Index bottomed at 18,056 on 4 June, the index has been unfolding a potential slanted double top formation with the neck-line passing through 18,850. The index completed the slanted double top formation by closing at 19,025 under the neckline in a long dark candlestick, off an intraday high of 19,357 today. With the breakout from the neckline in a long dark candlestick and WLPR (a momentum indicator) heading towards the bottom of the oversold zone, we expect more downside for the index. Based on the double-top formation, the index is likely to test the support at 18,483 near the 0.764x retracement level before bouncing back. On the other hand, if the index fails to find support at 18,483, it will see increasing odds to head towards the previous low of 18,056. Source: HKET Net

Important Disclosure We have based this document on information obtained from sources we believe to be reliable, but we do not make any representation or warranty nor accept any responsibility or liability as to its accuracy, completeness or correctness. Expressions of opinion contained herein are those of UOB Kay Hian (Hong Kong) Limited only and are subject to change without notice. Any recommendation contained in this document does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. This document is for the information of the addressee only and is not to be taken as substitution for the exercise of judgement by the addressee. This document is not and should not be construed as an offer or a solicitation of an offer to purchase or subscribe or sell any securities. UOB Kay Hian and its affiliates, their Directors, officers and/or employees may own or have positions in any securities mentioned herein or any securities related thereto and may from time to time add to or dispose of any such securities. UOB Kay Hian and its affiliates may act as market maker or have assumed an underwriting position in the securities of companies discussed herein (or investments related thereto) and may sell them to or buy them from customers on a principal basis and may also perform or seek to perform investment banking or underwriting services for or relating to those companies. UOB Kay Hian (U.K.) Limited, a UOB Kay Hian subsidiary which distributes UOB Kay Hian research for only institutional clients, is an authorised person in the meaning of the Financial Services and Markets Act 2000 and is regulated by Financial Services Authority (FSA). In the United States of America, this research report is being distributed by UOB Kay Hian (U.S.) Inc (“UOBKHUS”) which accepts responsibility for the contents. UOBKHUS is a broker-dealer registered with the U.S. Securities and Exchange Commission and is an affiliate company of UOBKH. Any U.S. person receiving this report who wishes to effect transactions in any securities referred to herein should contact UOBKHUS, not its affiliate. The information herein has been obtained from, and any opinions herein are based upon sources believed reliable, but we do not represent that it is accurate or complete and it should not be relied upon as such. All opinions and estimates herein reflect our judgement on the date of this report and are subject to change without notice. This report is not intended to be an offer, or the solicitation of any offer, to buy or sell the securities referred to herein. From time to time, the firm preparing this report or its affiliates or the principals or employees of such firm or its affiliates may have a position in the securities referred to herein or hold options, warrants or rights with respect thereto or other securities of such issuers and may make a market or otherwise act as principal In transactions in any of these securities. Any such non- U.S. persons may have purchased securities referred to herein for their own account in advance of release of this report. Further information on the securities referred to herein may be obtained from UOBKHUS upon request. UOB Kay Hian (Hong Kong) Research, Room 901 9/F, Aon China Building, 29 Queen's Road Central, Hong Kong Tel: (852) 2521 8787, Fax: (852) 2845 1655 http://research.uobkayhian.com MICA (P) 055/03/2012 RCB Regn. No. 198700235E

Technical Information Product: Acute Care Paste and Powder Acute Care Oral Paste and Supportive G.I. Powder were developed by Dr. Garry Pusillo. Dr. Pusillo is one of only a handful of board certified animal nutritionists in North America. Uniqueness, Applications and Uses: Acute Care Paste and Supportive G.I. Powder are unique oral supplements suitable for dogs, cats, rabbits, puppi

Cell Biochem Funct 2009; 27: 205–210. Published online 2 April 2009 in Wiley InterScience(www.interscience.wiley.com) DOI: 10.1002/cbf.1557In vitro effects of 2-methoxyestradiol on cell numbers, morphology,cell cycle progression, and apoptosis induction in oesophagealcarcinoma cellsVeneesha Thaver 1,2, Mona-Liza Lottering 2, Dirk van Papendorp 2 and Annie Joubert 2*1Department of Physiology,

Retail Market Monitor (Hong Kong)

Retail Market Monitor (Hong Kong)  Technical Analysis

Technical Analysis